Cumulative

Non-Cumulative

Understanding the difference between the two is critical for landlords, tenants, attorneys, and property managers to budget, bill, and negotiate leases fairly.

The Key Difference: Compounding Effect

Feature

Cumulative Cap

Non-Cumulative Cap

Cap Effect

Increases compound over time like a staircase.

Cap resets every year—only applies to that year.

Tenant Protection

More generous to the landlord over time.

More protective for the tenant year by year.

Landlord Recovery

Allows landlord to catch up on prior year shortfalls.

Landlord cannot recover unbilled increases from past.

Example Year 3 Cap Based on Year 1

105% x 105% x 105% = ~115.8% of Year 1 (compounded)

Still only 105% of Year 2 (not compounded)

A Simple Example

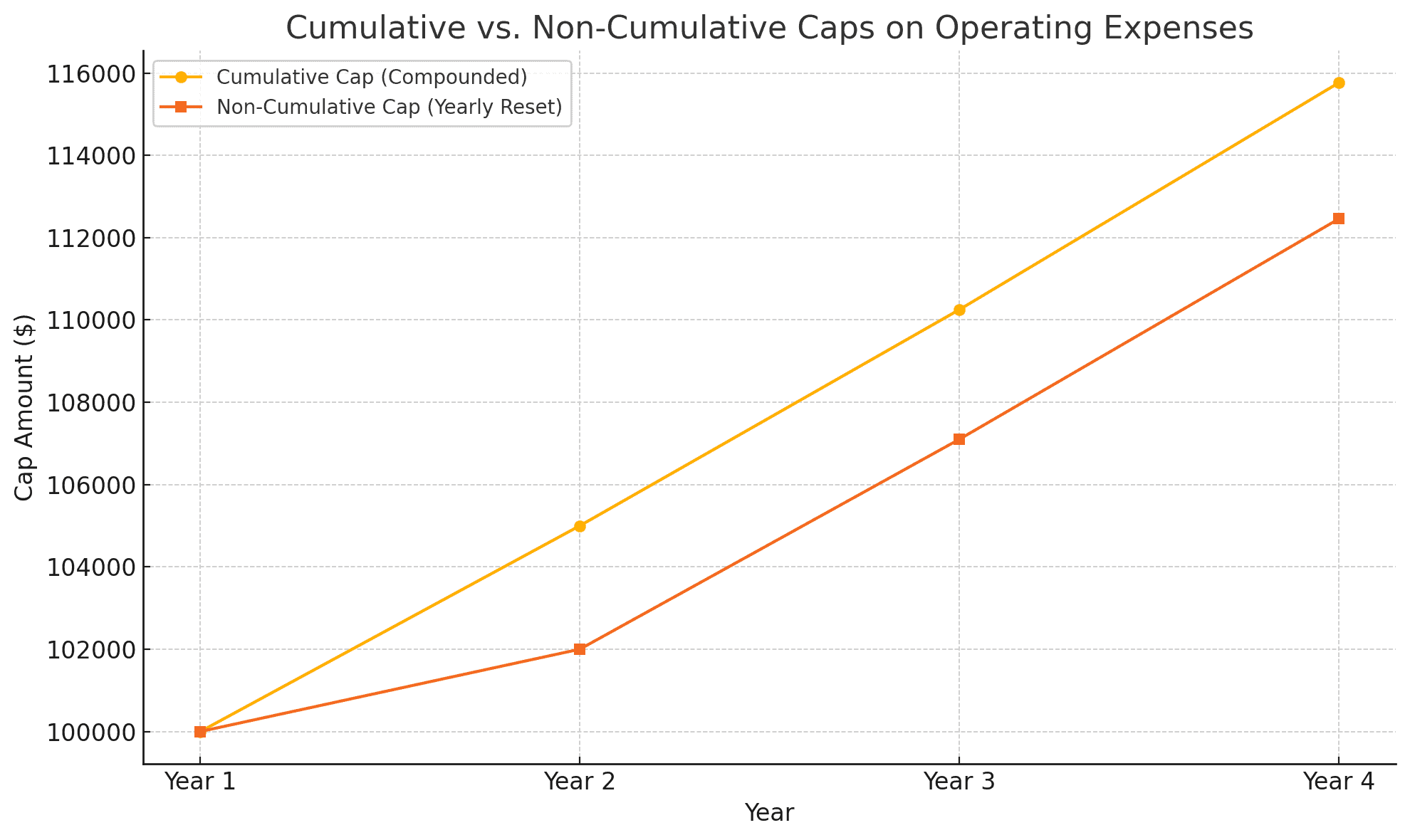

Let’s assume the tenant pays $100,000 in reimbursable CAM expenses in Year 1.

Scenario A: Cumulative 5% Cap

Each year, the cap compounds:

Year 2 Max: $100,000 × 1.05 = $105,000

Year 3 Max: $105,000 × 1.05 = $110,250

Year 4 Max: $110,250 × 1.05 = $115,762.50

So by Year 4, the landlord could charge up to $115,762.50.

Scenario B: Non-Cumulative 5% Cap

Each year, the cap resets based on the prior year only:

Year 2 Max: $100,000 × 1.05 = $105,000

Year 3 Max: $105,000 × 1.05 = $110,250

Year 4 Max: $110,250 × 1.05 = $115,762.50

So… they look the same?

Nope! Here’s the catch—what if the landlord didn’t increase the expenses to the max in a prior year?

Catch-Up Limitations

Here’s where it gets interesting.

Imagine in Year 2, actual charges were only $102,000 (under the cap):

Under a Cumulative Cap:

In Year 3, the landlord can still bill up to the compounded cap:

Year 3 Max: $110,250 (even if Year 2 was underused)

Under a Non-Cumulative Cap:

Year 3 is now limited to just 105% of $102,000, not Year 1:

Year 3 Max: $102,000 × 1.05 = $107,100

So the landlord loses the unused room to increase expenses. It does not carry forward.

Why It Matters for Property Managers and Accountants

Cumulative Caps require tracking prior years’ billed amounts and allowable increases to ensure landlords don’t exceed the total compounded cap.

Non-Cumulative Caps are easier to administer but limit recoverable costs if the landlord keeps increases low early on.

Audit & Compliance: You need clear records to demonstrate that cumulative increases are calculated correctly and to avoid disputes.

Budgeting: Knowing which cap type applies helps your team budget CAM recoveries more accurately year over year.

Final Tip: Look for “Cumulative Basis” in the Lease

If you see language similar to this:

“…shall not exceed one hundred five percent (105%), on a cumulative basis, of the portion of Tenant’s Additional Rent attributable to Common Area Expenses payable by Tenant for the previous year.”

| Year | Cumulative Cap (Compounding) | Non-Cumulative Cap (Reset Each Year) |

|---|---|---|

| Year 1 | $100,000 | $100,000 |

| Year 2 | $105,000 | $105,000 |

| Year 3 | $110,250 | $102,000 × 1.05 = $107,100 |

| Year 4 | $115,762 | $107,100 × 1.05 = $112,455 |